Media contact: Jim Bakken, jimb@uab.edu

Will Ferniany, Ph.D., is CEO of the UAB Health System, a more than $3 billion/year system that serves patients across Alabama and beyond, and includes the Viva Health Insurance Plan and the 19th-largest hospital in the nation, a safety-net hospital that sees more than a million patient visits a year and many of the most critical in the Southeast.The Affordable Care Act, commonly referred to as “Obamacare,” is flawed. It was based on a broken health care system and rushed into law. While there have been some positive outcomes, there have also been significant unintended consequences. Unfortunately, efforts to “Repeal and Replace” to date have been a modification of the broken ACA and similarly rushed, resulting unpassable legislation that can only be described as “Repeal and Make Worse.”

Will Ferniany, Ph.D., is CEO of the UAB Health System, a more than $3 billion/year system that serves patients across Alabama and beyond, and includes the Viva Health Insurance Plan and the 19th-largest hospital in the nation, a safety-net hospital that sees more than a million patient visits a year and many of the most critical in the Southeast.The Affordable Care Act, commonly referred to as “Obamacare,” is flawed. It was based on a broken health care system and rushed into law. While there have been some positive outcomes, there have also been significant unintended consequences. Unfortunately, efforts to “Repeal and Replace” to date have been a modification of the broken ACA and similarly rushed, resulting unpassable legislation that can only be described as “Repeal and Make Worse.”

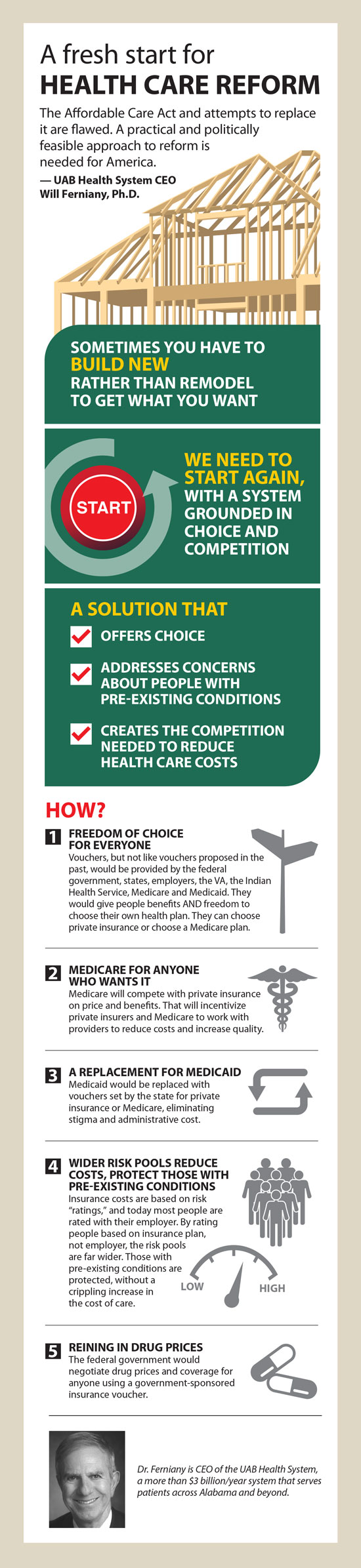

Working to improve the inherent flaws of the Affordable Care Act is much like doing extensive home renovations when the underlying structure of the house is bad. Many times, it is best to tear down the house and start with a new structure that can satisfy the needs of the homeowner, rather than spend time and money only to be unhappy. We cannot get to the system Americans need and deserve by modifying the flawed Affordable Care Act.

If lawmakers do not start fresh and build a system for America’s future, everyone’s best efforts and intentions will fall flat. We must improve the efficacy of the system to benefit patients, as well as make health care financially sustainable.

Following is a practical and (what I believe to be a) politically feasible approach to U.S. health care reform.

The keys to this solution are vouchers (for choice) and allowing everyone an option to purchase a Medicare solution. The proposal provides freedom of choice for people purchasing insurance; addresses concerns regarding pre-existing conditions; provides competition, thereby reducing the cost and increasing benefits; stabilizes the small and individual markets; ensures fairness by having large risk pools; and eliminates the Medicaid stigma barrier. We already have a proven example of how a voucher system could operate with Medicare Advantage, where beneficiaries can stay with traditional Medicare or elect private insurance. The private insurance companies compete to offer the best benefits for the “voucher.”

This proposal does not provide for universal insurance, but it does offer a foundation for such in the event that the federal and/or state government(s) wished to extend benefits to all, through tax credits or subsidies.

This proposal does not provide for universal insurance, but it does offer a foundation for such in the event that the federal and/or state government(s) wished to extend benefits to all, through tax credits or subsidies.

Medicare: Medicare would remain and would offer coverage options to all those who select it, and compete with private insurance. All people eligible for Medicare would be given a choice — to enroll in traditional Medicare, to enroll in a Medicare Advantage plan, or to use a voucher priced to the cost of traditional Medicare to purchase private insurance on their own.

Medicaid and Children’s Health Insurance Plan: Medicaid and CHIP as we know them would go away. States would decide the eligibility, voucher amount and minimum benefits for their residents. A federal match could remain similar to what it is today, where the federal government agrees to match at varying rates per state the money appropriated by the state for covering its Medicaid population. That said, the federal government could choose to move to a per capita funding model for states (where they agree to provide to states a set amount annually on a per enrollee basis), or to a pure block grant funding model (where they agree to provide to states a set amount annually without regard to the number of Medicaid enrollees in a particular state). With this approach, the stigma associated with having a “public” Medicaid card would be alleviated or eliminated. This coverage could be used with a private company or a Medicare product, and private insurers selling to Medicaid enrollees would be certified by each state’s insurance commissioner. There would be a minimum eligibility and benefit required for any state receiving a federal match for sponsoring Medicaid/CHIP-eligible people.

Large and Small Employers: Employers would stop purchasing policies directly for their employees, but rather provide vouchers, and employees would be able to use the voucher for a private policy or a Medicare offering. Employees would have freedom of choice on their policy, and if the chosen policy is less than the voucher, the remaining balance would be placed in a health savings account for that employee’s benefit. Instead of being rated by the employer, a plan’s ratings would be determined by all people purchasing the insurer’s products. Employers could work with insurers and Medicare to provide offerings based on their voucher amount and make these choices available to employees. They would have to offer plans from at least three insurers and Medicare.

Individuals: Those obtaining insurance as individuals would continue to purchase insurance or buy a Medicare product. They would be rated with all other customers buying from that insurer. Individuals eligible for a subsidy or tax credit would be determined off the exchange by applying to the state Public Health Department based on criteria determined by the federal government, which would fund the subsidy or tax credit. This system would eliminate the need for an insurance mandate or penalty, as well as concerns about religious issues.

Insurance Companies: To attract customers, insurers would compete with each other and Medicare to try to reduce cost with providers as much as possible, and increase quality to offer the best benefits to the voucher customers (similar to Medicare Advantage today). Insurers would be certified to offer coverage by the state insurance commissioner. Ratings would be based on all those covered by the insurance company, not by individual groups or segments. Insurance companies have some marketing restrictions on the individual market similar to but less than Medicare Advantage to prevent the company from “cherry picking” those who select their company. The plan could include a “risk adjustment” provision as in the Affordable Care Act.

Veterans, Department of Defense, Indian Health Service: Each would remain, and those currently eligible could continue to receive services in these facilities. All people eligible for these services would be given a choice — use the government-sponsored system or use a voucher priced to the cost of traditional services to beneficiaries to purchase insurance on their own.

Drug Prices: The federal government would negotiate drug prices and formulary for all persons purchasing insurance in America through a government-sponsored or subsidized voucher. Private companies would have the option of utilizing these prices and formulary or negotiating their own.

It is possible to balance compassion with good business sense and fiscal responsibility in health care reform. A foundation like the one outlined here — with the right amount of good-faith debate and insight from other experts — could lead to that very outcome.