The term trainee payments is used by the University, but defined by the IRS as a fellowship payment. Fellowship payments have specific tax reporting requirements for federal and Alabama state filings. The following are points that you should consider when completing the required tax documents.

- Trainee/Fellowship payments are not reported to any tax agency.

- Exception: Trainee/Fellowship payments made to a NRA with NRA Tax ramifications are subject to 1042S reporting requirements. NRA Tax is identified on your payslip.

- Exception: Trainee/Fellowship payments made through UAB Payroll Services to UAB students are reported on the 1098T form provided there were tuition, scholarship or other qualified payments posted to the student account. This information is reported to the IRS. The 1098T is issued by UAB Student Accounting.

- Trainee/Fellowship payments made to US citizens or RA taxed as U.S. citizens are reportable to the federal government.

- Trainees in this category should retain their 31DEC20XX payslip for a record of the year-to-date information. Copies of payslips may be accessed through Oracle Self Service. Download instructions for accessing payslips.

- Assistance in determining how to report these payments is available in most online filing software.

- Following is the information on where to report fellowship payments on the 1040 Internal Revenue Service Forms as defined by IRS publication 970.

- Trainees in this category should retain their 31DEC20XX payslip for a record of the year-to-date information. Copies of payslips may be accessed through Oracle Self Service. Download instructions for accessing payslips.

How to Report (Federal)

How you report any taxable scholarship or fellowship income depends on which return you file.

- Form 1040EZ. If you file Form 1040EZ, report the taxable amount on line 1. If the taxable amount was not reported on Form W-2, enter "SCH" and the taxable amount in the space to the left of line 1.

- Form 1040A. If you file Form 1040A, report the taxable amount on line 7. If the taxable amount was not reported on Form W-2, enter "SCH" and the taxable amount in the space to the left of line 7.

- Form 1040. If you file Form 1040, report the taxable amount on line 7. If the taxable amount was not reported on Form W-2, enter "SCH" and the taxable amount on the dotted line next to line 7.

This information is taken directly from the Alabama Administrative Code (810-3-14-.02 Exclusions from Gross Income).

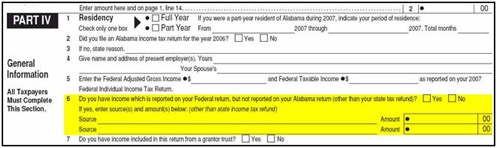

How to Report (State of Alabama)

As for reporting the income, the State of Alabama tax form does require disclosure of the payments, but they should be qualified as scholarship/fellowship payments. The graphic below shows the line on which the payments should be reported (Part IV, line 6).